Summary

Aimmune published highly robust Phase 3 (RAMSES, ARTEMIS, and PALISADE) data for AR101. Therefore, the drug is positioned to gain FDA approval for treating peanut allergy by January 2020.

Nonetheless, ICER recently issued a report that questioned the utility of desensitization therapies for peanut allergy.

As opinions rather than facts, the ICER statement is a theory that is used to generate discussion. As such, they do not have any material impact on AR101's approval.

This idea was discussed in more depth with members of my private investing community, Integrated BioSci Investing. Get started today »

The stock market is designed to transfer money from the active to the patient. - Warren Buffet

In bioscience investment, it's crucial to filter out opinions from facts. Despite that you hold a fundamentally sound company, you will face streams of negative market opinions. To stay grounded, it's imperative for you to conduct research due diligence to know when the news is simply a "head fake." This phenomenon is best epitomized by the investment thesis on a food allergy innovator dubbed Aimmune Therapeutics (AIMT).

Though Aimmune delivered extremely robust clinical outcomes for the Phase 3 (RAMSES, ARTEMIS, and PALISADE) trials, its desensitization therapy has been the subject of market negativity. The latest discussion originated from the Institute for Clinical and Economic Review. Notwithstanding, the intelligent Aimmune shareholders are undeterred because such news is simply opinion rather than fact. In this research, I'll present a fundamental analysis of Aimmune while dissecting the negative arguments.

Figure 1: Aimmune chart (Source: StockCharts)

Figure 1: Aimmune chart (Source: StockCharts)About The Company

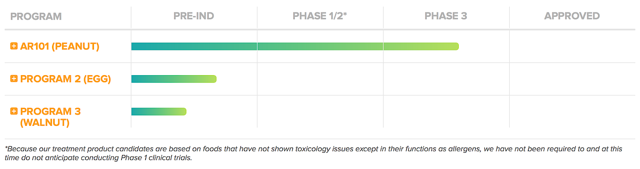

As usual, I'll deliver a brief corporate overview for new investors. If you are familiar with the firm, I suggest that you skip to the subsequent section. Headquartered in Brisbane California, Aimmune Therapeutics is focused on the innovation and commercialization of medicines to serve the food allergy market. As the crown jewel of the pipeline, AR101 is an oral biologic for peanut allergy. Designed by the characterized oral desensitization immunotherapy (i.e. CODIT) platform, AR-101 is a powerful preventative (i.e. prophylactic) therapy. Asides from AR101, Aimmune is expanding its development to serve the unmet needs in other food allergies such as egg and walnut.