Summary

Intercept is an excellent contrarian bet due to a stream of negative news flow amid the strong fundamental development. As such, there is definitely a silver lining in the dark.

The current pessimism against Intercept is the 2019 NASH draft guidance. Mr. Market believes that the draft will hamper the prospect of obeticholic acid's approval. This is certainly overblown.

As the light that shines in the darkness, the Phase 3 REGENERATE trial for obeticholic acid covers all bases. With strong data, OCA will gain approval for all NASH stages.

You only have to do very few things right in your life so long as you don't do too many things wrong. - Warren Buffett

In Benjamin Graham's book The Intelligent Investor, the Father of Value Investing epitomizes the fickle nature of the equity niche as "Mr. Market." Driven by emotion, Mr. Market usually makes impulsive decisions that are disconnected from the stock's fundamentals. His mood is reflective of a pendulum that swings to either extreme optimism or grave pessimism. As I'm cognizant of his behavior, I'm enthused by a good investment prospect disdained by Mr. Market. In my view, investors have a much better chance of uncovering undervalued equities during a stock's period of unpopularity. If all experts are opining positively on a stock, chances are that it's either optimally priced over overpriced. A prime example of this phenomenon is Intercept Pharmaceuticals (ICPT).

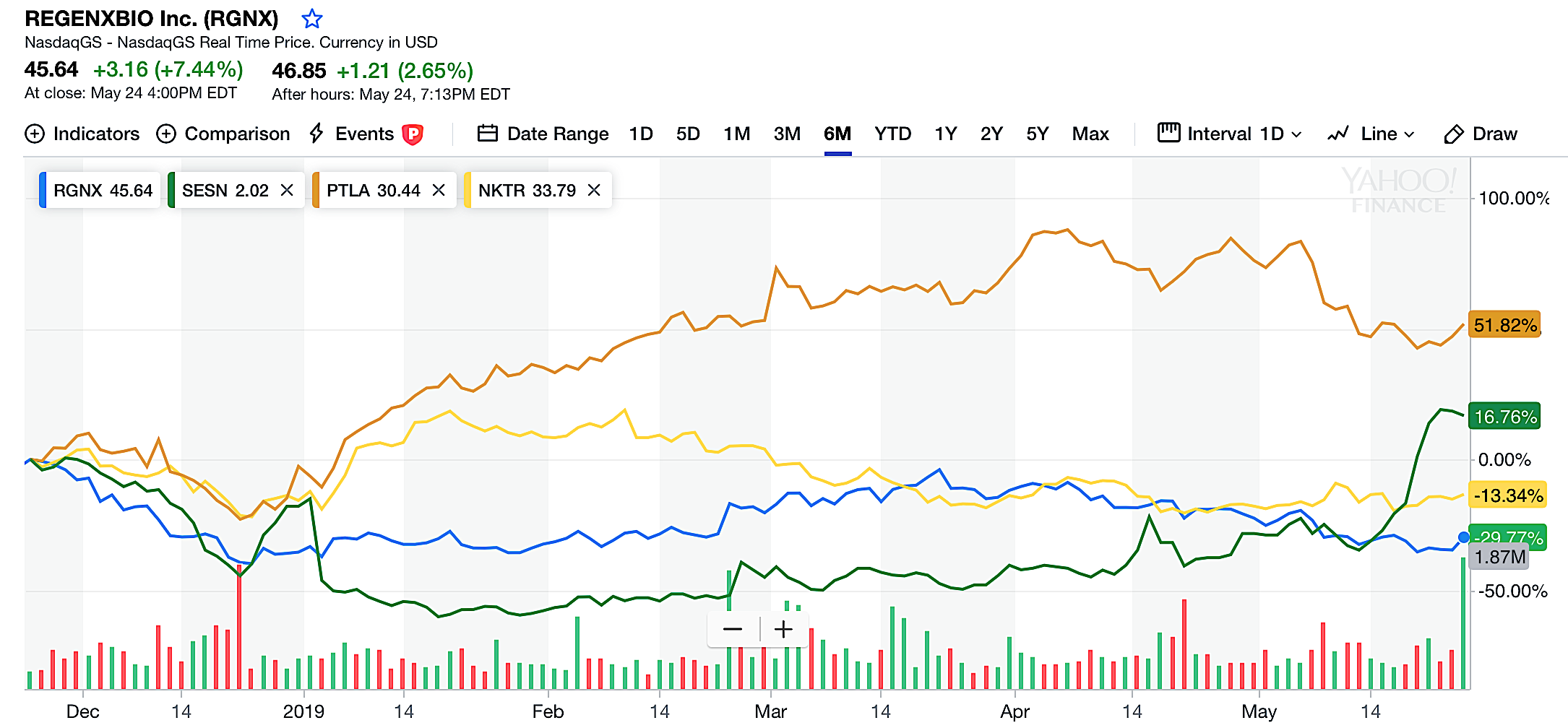

Figure 1: Intercept chart (Source: StockCharts)

Figure 1: Intercept chart (Source: StockCharts)

The current market consensus believes that there are irreparable safety issues centering the lead medicine obeticholic acid (Ocaliva). Nonetheless, OCA is already approved for another liver disease for years. Therefore, it's acceptable safety profile is established. As I addressed those specific issues in prior articles, I'll defer from going over the same issues. That aside, it seems that Mr. Market is now having a fit regarding the latest FDA guidance for nonalcoholic steatohepatitis ("NASH"). Despite the grim outlook, the fundamental picture of Intercept is brighter than ever. In this article, I'll present a fundamental analysis of Intercept while focusing on the ramification of the FDA draft guidance.

About The Company

As usual, I'll deliver a brief corporate overview for new investors. If you are familiar with the firm, I suggest that you skip to the subsequent section. Headquartered in New York City, Intercept is focused on the innovation and commercialization of a semisynthetic bile acid known as OCA to treat serious liver conditions. In binding to the “holy grail” receptor farnesoid X, OCA activates many key regenerative responses. On May 2016, the FDA approvedOCA as Ocaliva for the treatment of a rare and chronic liver condition, primary biliary cholangitis ("PBC").

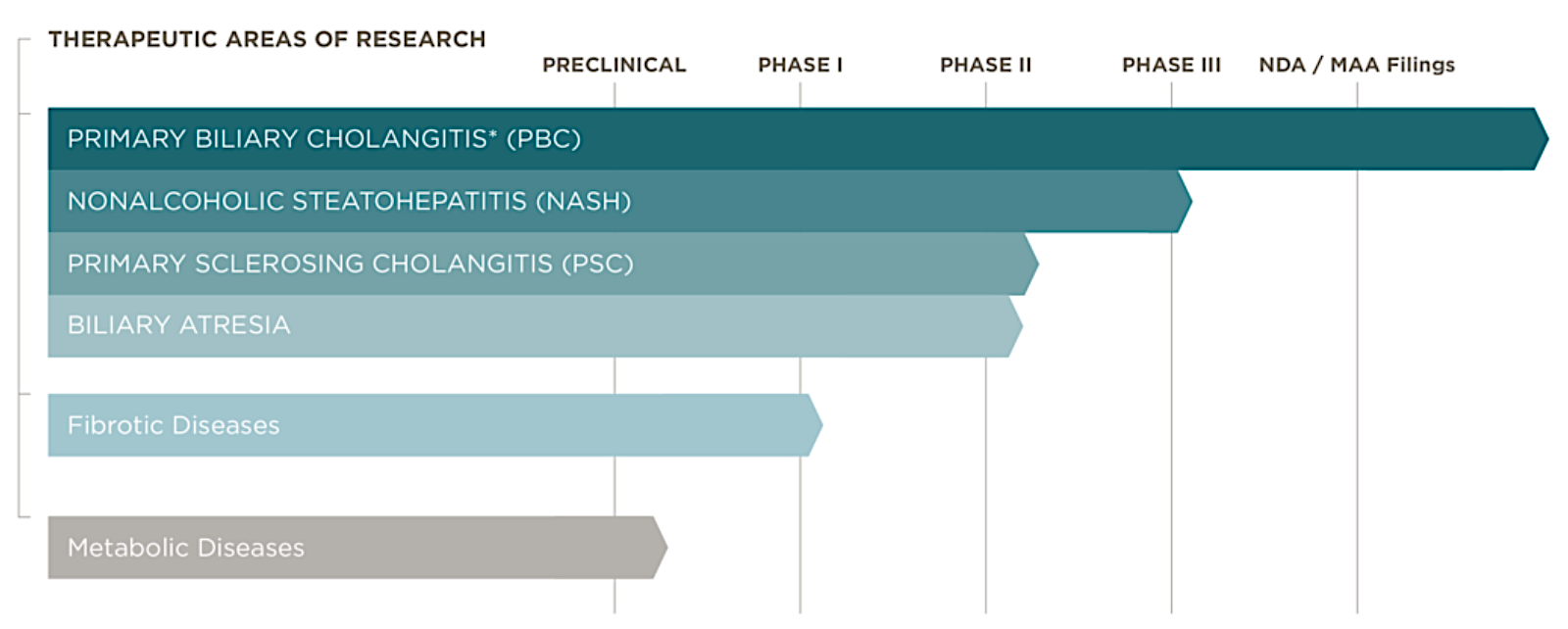

Figure 2: Therapeutics pipeline (Source: Intercept)

Figure 2: Therapeutics pipeline (Source: Intercept)

Currently in a Phase 3 trial, Intercept is most likely the first company to launch a medicine for managing the highly prevalent fatty liver disease, NASH. As the crown jewel of Intercept is its fatty liver disease franchise, I'll shift gears to cover the recent market concern regarding NASH.